A story and simple math: (What You Care About) X (Smart Investment Tools) = Making An Impact

As a former girl, I’m passionate about girls’ education.

Growing up, I was inspired by my single mom’s struggles and sacrifices to pursue a nursing degree in mid-life. I had limited guidance in figuring out how to pursue my own university education. But I was one determined teenager. I figured out financial aid and was accepted at a leading U.S. private university.

It changed everything.

So when I hear the stories of girls all over the world and the even crazier hoops they have to jump through to receive an education, I have to jump through hoops for them.

Because I know it will change everything.

For them, their families, communities and countries.

What is it that you care deeply about—and why?

This is the first and most important question. We can’t get into the math that is the topic of this article without that variable.

As an investor, I believe girls’ education is the world’s best investment.

After graduating with a degree in math, I spent 22 years working in the investment industry—Wall Street to West Coast.

The biggest thing I learned?

A good investor is comfortable investing in imperfection—the developing country, the company in transition. She chooses the investment because she believes in the thesis. She diversifies because a thesis never works out as hoped.

Good investors make sure they’re maximizing every dollar invested—minimizing fees and taxes, maximizing return and impact—whatever that means for them.

When I took the CliftonStrengths assessment, I wasn’t surprised which of the 34 strengths was my most dominant. I’m a Maximizer.

Was I pulled to investing because of my strength, or did working in the investment industry develop my strength?

It’s probably a bit of both—nature and nurture.

I’m a global investor and connector. I know the power of maximizing capital—both financial and social.

Now we are ready for the math.

The story of how $100 in my investment account sent 18 girls to university breaks into four parts:

- Investing in what I believe in

- Having plans—investing, charitable, tax, legacy

- Being savvy about investment tools to maximize each dollar

- Seeing money not as the end goal, but a tool for impact

Let’s explore each of them.

1. Invest In What You Believe In

My portfolio emphasizes investments outside of the U.S. (including developing economies) and under-invested segments (like women’s health).

I invest in what I believe in.

Like many in the U.S., a large part of my taxable investments are in U.S. stocks. I use an investment manager to manage a portfolio of individual stocks that looks and feels like the S&P 500 Index, but has a basic gender lens—for example, every company has at a bare minimum at least one woman on it’s board.

I think that’s a pretty basic hurdle.

It’s traditional investing, but done a way I believe in.

2. Having plans—investing, charitable, tax, legacy

My U.S. stock investment manager is tax-aware—across positions, they harvest losses and minimize taking gains. The “good problem” after years of market returns? I’m sitting on sizable gains in tech stocks like Nvidia, Apple, Microsoft.

It’s a great time to trim my winners. But doing so comes with a (tax) cost.

But I don’t have to sell share. I can gift them—and earn an immediate tax deduction and avoid paying capital gains tax. And the winnings go towards my charitable strategy to fund girls’ education.

I ask my investment manager to recommend which shares to gift. The consistent answer? Nvidia. Every $100 of Nvidia I’ve held for a decade is now worth $10,000.

Pulling these shares from my portfolio helps my manager rebalance it. I lock in an incredible gain. I reduce my current year tax burden.

Most importantly, I fund girls going to school. Girls’ education is the focus of my charitable giving and legacy.

I’ve got big plans for this one impactful life. This is how investing, tax, charitable, and legacy strategies all come together to support it..

3. Be savvy about investment tools to maximize each dollar

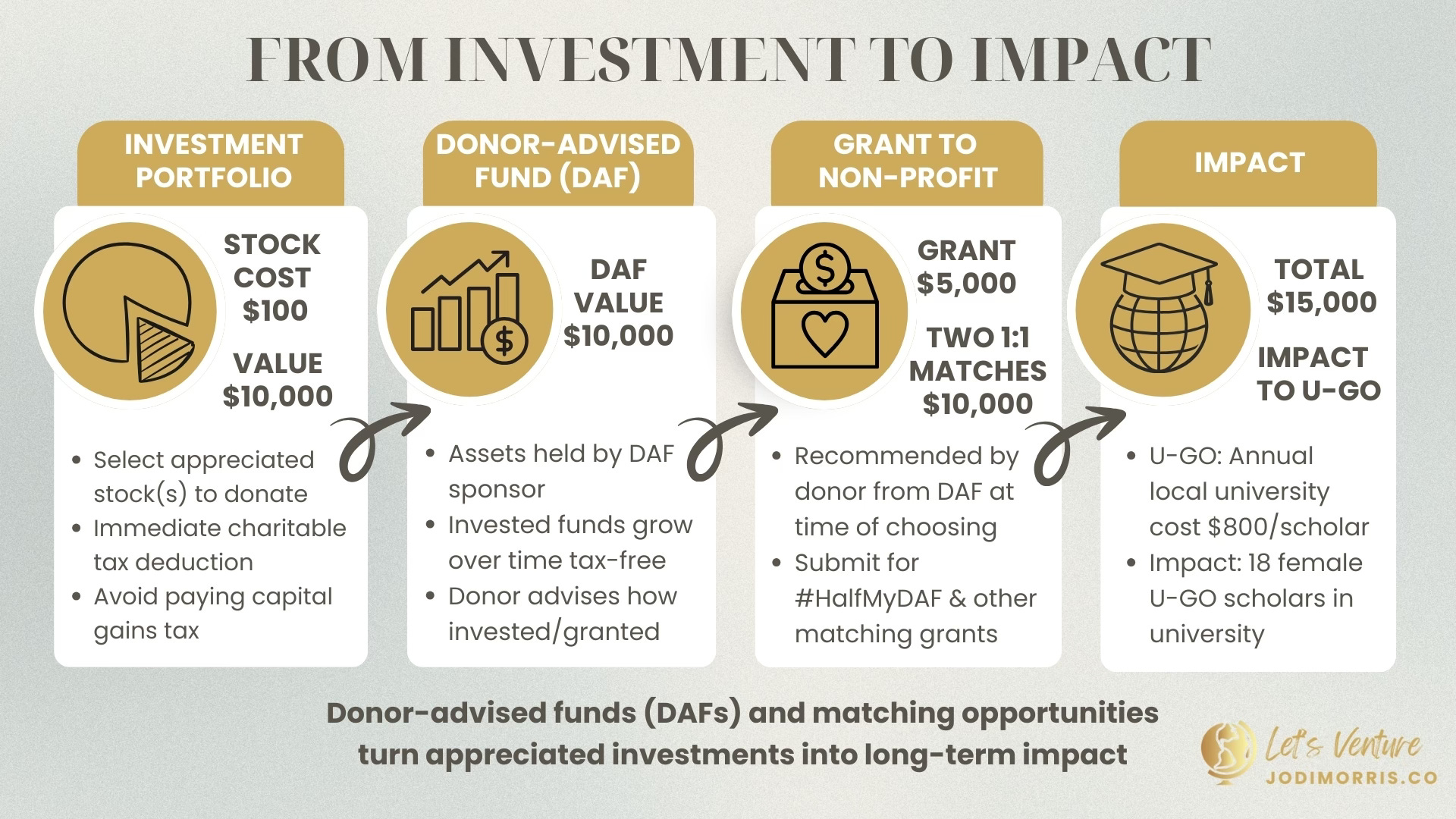

That $10,000 didn’t go to one non-profit, but to my donor-advised fund (DAF)—held at DAFgiving360, itself a charitable organization.

DAFs. are one of my favorite financial tools—and among the most under-utilized. I write about them and have coached countless smart, charitably-minded friends on how to use them. Financial advisors might not be fully versed or incentivized to suggest a strategy that encourages their client to give their money away today.

I give them the questions to have that conversation.

The basics? A donor-advised fund (DAF) is a charitable giving account that allows you to donate assets and receive an immediate tax benefit. While you know longer own the assets, you advise how the funds are invested (tax-free growth) and recommend grants from the DAF to the non-profits you care about at the time of your choosing.

It’s a way to separate the tax benefits of charitable giving from the choice and timing of granting decisions.

But here’s the biggest thing.

Having a donor-advised fund changes your mindset.

With the money given away, you get serious. Since opening my DAF, I formalized five girls’ education non-profits as partners—each emphasizing a unique angle I believe important. With each, I’ve clarified how to invest both my social and financial capital.

The one big risk with DAFs? That people don’t have a strategy and hoard tax-advantaged funds in an account.

I am constantly reminded that talent is universal, but opportunity is not. There are millions of girls who deserve to be in secondary school and university—to all our benefit.

That’s all the incentive I need.

Fortunately, a savvy group of people also worry about the $326 billion currently sitting in DAFs—and are doing something about it.

HalfMyDAF inspires donor-advised fund holders with a great incentive—a $2 million pool of matching funds for DAF holders who commit to spend down at least half the funds in their DAF during the year.

It’s simple. I make grants, submit them, and in June and October HalfMyDAF hosts random drawings in which grants are selected for 1:1 matches up to $5,000 each– with four lucky nonprofits receiving matches up to $25,000.

I love campaigns that drive me to action.

I grant $5000 to girls’ education non-profit U-GO. It’s selected for a HalfMyDAFmatch. Sending an email to U-GO with news of the matching grant makes my day.

Speaking of matching, make sure you maximize all matching opportunities—from your (and spouse’s) employer, and campaigns from the non-profit itself. You might need to modify the amount or timing—but the 100% return is worth it.

4. Seeing money not as the end goal, but a tool for impact

Let’s recap on our simple math.

- My original $100 invested in Nvidia became $10,000, which I gift to my DAF.

- Months later, I grant half of it ($5000) to girls’ education non-profit U-GO.

- The $5000 grant is selected for matching by HalfMyDAF.

- It’s matched again by another campaign.

- The $5,000 grant becomes $15,000 (with the remaining $5000 still growing in my DAF, for this same process to be repeated over the next few years)

- Per U-GO, $800 sponsors a young woman for a year of university. That means $15,000 equates to 18 scholars attending a year of university.

Today, 18 girls are in school because of $100 invested a decade ago and some smart investing and matching strategies. To me, that is impact.

I end this with the obvious disclaimer that while this is a real-life example, it will not be everyone’s (or my) example in the future.

Is it everyday that one holds a stock that a decade later is worth 100x its cost?

No. The prior decade has been an exceptional period, particularly for certain tech stocks. I have several others that are up 10-20x. Check your portfolio, you might, too.

The point is the multiplier effect. There’s a “rule of 72” that is shorthand for how long it takes for your money to double—if the market goes up 8% a year, it takes 9 years. If you invest across a diversified portfolio of holdings (stocks, funds) and seek to minimize fees and taxes, you maximize the chance of that happening.

Are DAFs only for wealthy individuals?

DAF providers all set different minimums, but major firms like Schwab (DAFgiving360) and Fidelity have no DAF account minimums. With a DAF, I rarely make a charitable contribution with cash. It allows me to give many times more over my lifetime.

My husband and I seeded DAFs for nieces and nephews as college graduation gifts. It forces a whole conversation on investing, taxes and charitable giving. When they make a gift to their DAF to take advantage of their employer’s annual match, I smile.

Will your grant always be matched?

HalfMyDAF operates by random drawing. While not all of my grants get matched, I’ve gotten pretty lucky. And if my grant is not selected, perhaps the friend I referred to the campaign’s grant was. That’s impact, too!

HalfMyDAF incents me to make grants earlier in the year. November and December remain the race-to-the-finish for most non-profits (and when many sponsor matching grants). Grants made early in the year are met with a hearty thank you.

Finally, remember that. you can BE the match! For example, set up a campaign around your next birthday, matching contributions up to a certain amount. It’s an excuse to share the story of your favorite non-profit with family and friends, and why it’s meaningful to you.

I took you through some simple math:

(What You Care About) X (Smart Investment Tools) = Making An Impact

The hardest is the first variable—what is it that you care deeply about, and why?

Spend the time here. I promise that with a clarified mission, you’ll continually find the savvy people and tools that further your impact beyond what you dreamed possible.

Stories and math are my favorite combination. My mission is connecting people and ideas so that we each maximize our impact. If you need a partner to help work through your own, I’d love to hear how I can support as a Success Coach.

Discover more from Jodi Morris

Subscribe to get the latest posts sent to your email.